While the largest diversified funds still rule the pack, capital is increasingly flowing to vehicles with a singular investment focus.

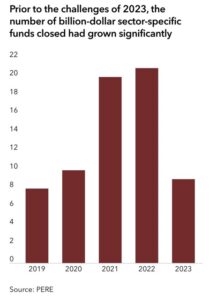

Off the back of the worst year for private real estate fundraising since 2012, managers running the 1,280-plus closed end funds PERE is tracking in market at the start of 2024 will be hoping for better.

Their challenge? Standing out in a congested backlog of vehicles currently seeking $417 billion in commitments from an institutional investor pool that has largely had its hands tied by issues including the denominator effect and a lack of distributions from existing outlays. Per PERE data, this figure is up 40 percent on one year prior, and represents the largest January total on record.

Despite this fundraising logjam, PERE’s Perspectives 2024 Study found 39 percent of investors are looking to inject fresh capital into the asset class in the coming year. The sector specialists are set to be key beneficiaries of this.

Indeed, PERE data also reveals an uptick in the proportion of capital directed to sector-specific real estate funds post-covid. In both 2022 and 2021, single-sector funds were responsible for 38 percent of total capital raised for closed-end funds, up from an average of 24 percent for the years 2018-20. In those two years, 41 single-sector funds each closed on at least $1 billion.

Momentum stalled in 2023, however, with sector-specific vehicles attracting 23 percent of the $129 billion in capital raised by closed-end funds. But in a challenging year that saw capital highly concentrated in just one mega-fund, this proportion jumps to 30 percent if Blackstone Real Estate Partners X – the $30.4 billion behemoth and only fund that managed to surpass the $5 billion mark – is removed from the mix.

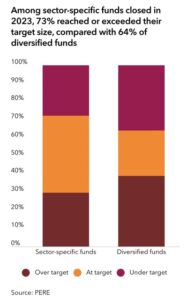

Both diversified and sector-specific funds struggled to attract capital in 2023. But single-sector funds were more likely to achieve or exceed their target fundraise than their sector-agnostic counterparts. PERE data shows 73 percent of sector-specific funds closed met or exceeded their target size, compared with only 64 percent of diversified funds.

Specialists were also more efficient in attracting capital – a trend that has become markedly more pronounced in the past three years. The average time spent in market by sector-agnostic funds increased from 14 months for those closed in 2021 to 22 months in 2023, per PERE data. Conversely, the average for sector-focused funds increased only marginally from 13 to 15 months.

Steven Cowins, co-chair of the global real estate funds practice at law firm Greenberg Traurig, believes this fundraising momentum will continue. “There’s room in the market for both approaches. But I think it’s possibly easier in the current environment to raise capital for a sector-specific strategy, because investors will be able to look and feel more what they’ll be investing in,” he says.

To gauge how sector specialists will fare in 2024 – with those currently in market seeking to raise $115 billion in commitments – PERE connected with a number of investors, managers and advisers globally. Together they paint a nuanced picture of a fundraising market that, while increasingly bifurcated, is no less balanced.

Chasing alpha

The New Mexico State Investment Council, which derives its wealth from oil and gas revenues, made 10 real estate fund commitments in 2023, per PERE data. Three of these went to single-sector vehicles. Keith Sabol, asset class director for real estate and real assets, expects this approximate split between sector specialists and diversified funds to continue in 2024, with an expected real estate pacing plan north of $1 billion for the Santa Fe-based investor.

Screenshot

Because the pacing is large relative to its invested capital base, the portfolio has to be broadly diversified in terms of both sectors and geographies, he explains, with constraints on time and staffing additional factors driving the majority of the investor’s commitments to diversified funds, which are typically larger than single-sector funds.

However, given that diversified managers have their own opinions about the market segments and geographies that work for them, Sabol says sector specialists play two key roles in portfolio construction. “Specialty funds are a helpful tool for fine-tuning sector or geographic exposures,” he explains. In addition, they allow the sovereign fund to explore potentially higher alpha niches in the market.

Sabol says a single-sector exposure targeting alpha generation lends itself well to underdeveloped niches, such as public storage. “That sector was below the radar, maybe a decade or so ago, and now you’ve got multibillion-dollar public companies in the space,” he explains. Backing a niche sector at an earlier stage, however, typically means making a smaller commitment to a smaller fund, which is challenging for a large investor such as NMSIC to do.

But the investor does not rule this out. Last September, it approved a $100 million commitment to Alterra IOS Venture III, which was launched by Alterra Property Group in February 2023 with a target of $750 million for investment in US industrial outdoor storage assets.

Alterra had an emerging track record in the space, however, having raised $524 million for the predecessor fund in 2022, according to PERE data. “We like to see as much verifiable track record as possible, and we try to determine that it supports management’s thesis, and that we can also get behind the thesis and have a reason to believe there’s something about the process that makes it repeatable,” says Sabol. “The less competitive nature of the underdeveloped niches provides an opportunity for institutional-quality management teams to exercise their skills to great advantage.”

Perfect fit

For specialist managers of non-traditional property classes to attract capital from the largest investors, then, past performance is key. But there is another tailwind on their side.

Post-covid, real estate’s primary food groups of logistics, office, retail and residential have faced a toxic cocktail of structural headwinds compounded by a steep correction in values and a retrenchment in bank lending. Although all property sectors have been impacted by interest rate hikes, the degree to which this is hurting returns varies greatly. In the US, for example, the NCREIF Property Index measured total returns for 2023 of -17.6 percent from offices, compared with -7.3 percent for apartments and -4.1 percent for industrial. Hotels, on the other hand, generated 10.3 percent.

“Amid the economic uncertainty, an investor is going to be aware that some of the traditional property types have some real issues, and look at the new property types in growth sectors that allow them to really drive performance in a broader allocation pool,” says Mit Shah, founder and chief executive officer of Noble Investment Group, an Atlanta-based manager focused exclusively on select-service hotels across the US. The firm has just closed its fifth and largest commingled fund, raising $1 billion against an $800 million target.

Screenshot

“Investors are cherry-picking what they like and what they think will do well out of this repricing, and sector specialists will be the beneficiaries of that,” says James Jacobs, head of real assets advisory at capital advisory Lazard. “It’s not that the mega-funds don’t play in those sectors, but investors might want to just augment their exposure.”

To meet this need, Cowins observes a growing number of diversified managers in the market “trying to launch some sort of sector-specific vehicle.”

Data centers are a key recipient of attention here. With specific technical or operational expertise required, it shares some of the characteristics that make hospitality suited to a single-sector play. But as tenant demand for data center capacity explodes alongside the growth of the cloud and artificial intelligence, the ability to scale is a key advantage of a data center fund, PERE sources say.

“The size of data center properties today has increased significantly. Most leases to hyperscale tenants are 40MW in capacity or larger, which is resulting in very large single-asset exposures,” says John Berg, global head of private real estate at Principal Asset Management. “To construct a new facility of that size for a tenant today will cost $500 million or more in the US. You may be able to add one or two assets of that size in a large, diversified portfolio, but your exposure within that fund to the data center sector would be quite concentrated.”

The Des Moines-based firm has been investing in data centers for 17 years, mostly via diversified funds and separate accounts, but closed its first US data center-focused fund on $529 million in 2021, per PERE data. A European counterpart with around $300 million followed last year.

Berg says investors in the firm’s data center-focused funds tend to be large enough to move beyond exposure to the sector through diversified funds only, and see it “as a strategic and intentional overweight in their portfolios.”

Stockholm-based Areim is another diversified manager that has branched out into raising a dedicated data center fund. The Nordics-focused firm closed Areim DC Fund with €446 million last year. “Having made smaller investments in data centers through our third and fourth multi-sector funds, we realized we had trapped the huge growth potential of this sector into a maximum allocation with a finite life, as is typical for a diversified fund,” says Dietrich Heidtmann, head of global capital formation. “It was a very logical step to create a dedicated, more permanent vehicle in which we could combine all our data center activities into a single fund and raise additional capital specific to this opportunity.”

Smooth operators

Although most specialists in niche or underdeveloped sectors have yet to reach the scale of some of their diversified peers, nine single-sector funds did close on at least $1 billion last year. Three featured in the top 10 for the industry as a whole, per PERE data.

The largest single-sector fund – and the second-largest fund overall – closed in 2023 was the US-focused EQT Exeter Industrial Value Fund VI, which exceeded its $4 billion target to attract $4.9 billion. Philadelphia-based EQT Exeter primarily raises single-sector and single-geography funds across logistics, residential and office/life sciences, and manages around $29 billion in real estate assets.

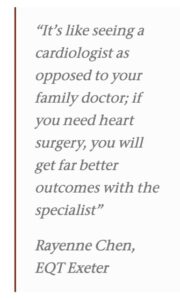

Rayenne Chen, partner, global client solutions at EQT Exeter, believes the firm’s sector-operator model can replicate the scale of a global diversified fund through multiple smaller, sector-focused funds, but achieve greater alignment of interest from the sector teams, more informed and granular investment execution, and better net margins. “It’s like seeing a cardiologist as opposed to your family doctor; if you need heart surgery, you will get far better outcomes with the specialist,” she says.

Evidently, investors are buying into this thesis. Each iteration in EQT Exeter’s US-focused industrial fund series, for example, has grown. The firm is also responsible for three of the 10 largest single-sector private real estate funds raised in the past four years, PERE data shows.

Compared to when the firm started out in 2006, Chen says sector specialization is much more widely accepted today. “Many institutional investors, especially those with less than $1 billion of assets under management, were reluctant to take the concentration risk, especially if they had only just begun to invest in real estate. Now, investors have achieved a diverse base and have, in many cases, doubled their portfolio allocation to real estate to 10 percent or more. So the universe of converted investors and available capital is substantially larger,” she explains.

Assessing the competition

EQT Exeter’s story is evidence the sector specialists are not impeded by the continued growth of the industry’s largest diversified managers. If anything, the mega-managers are indirectly helping the specialists to grow.

Indeed, Shah is keen to emphasize that Noble is not in direct competition with the diversified funds that allocate to hospitality. Instead, the increasing activity in the sector from the likes of Blackstone, Brookfield and Starwood helps to institutionalize it. “This gives ground to smaller managers to say we can build a mouse trap to take advantage of some of the dislocation, because these larger allocators can serve as buyers,” he says.

Screenshot

Shah also believes investors value a blend of both vehicle types in their portfolios. “I think about it as two ends of a barbell: you have the sharpshooting operator-focused strategy at one end, and the thematic global capital allocator at the other. One will be the first and last call on the multibillion-dollar opportunities that move capital markets, and Noble has been the first and last call on $50 million investments where we can deploy $20 million of equity at a time,” he says.

Jacobs agrees specialists are not competing with the largest diversified firms. “Specialists will continue to grow. But they’re not taking share from the mega-funds. They’re taking share from the mid-market generalists, which are really struggling today to find a purpose,” he says.

For Richard Peacock, European head of real assets equity at manager Aegon Asset Management, this trend is a sobering reality. His team, the UK and European real estate investment platform of the Aegon insurance group, is in the process of winding up operations. It raised two generalist vehicles between 2013 and 2017, sized at £200 million ($251 million; €233 million) and £150 million, and recently closed its UK open-end fund.

“I think anyone trying to raise money these days for a general balanced strategy is up against it, frankly. From an equity-raising perspective, specialism is absolutely essential,” he says. “This is a response to the polarization we’re seeing between the winners and losers in terms of the sectors that have structural tailwinds. It’s also a recognition that properties in operational asset classes require partnerships between landlord and customer – they require a deep level of expertise and understanding of your customer.”

Even though the largest managers are raising significant amounts of capital for diversified strategies, Peacock believes they have evolved into pseudo-specialists. “Even in a diversified wrapper they’re still only going to do logistics, data centers, life sciences and sectors they’ve got conviction on,” he says. “I just cannot believe that you can raise money today without giving your investors some kind of idea of what might go into this portfolio.”

A winning combination

Marten Foxon, who until late 2022 managed the global hospitality portfolio of Abu Dhabi Investment Authority, agrees even a large, $5 billion generalist real estate fund “doesn’t really wash anymore” with sophisticated institutional investors. “They are thinking more specifically about where and how their capital will be deployed.”

Foxon says ADIA’s more targeted strategy led the sovereign investor to concentrate capital in specific asset classes including logistics, multifamily and hospitality where it had the most conviction. This included re-upping with trusted specialists, particularly in Asia-Pacific, where there is a greater trend among managers to specialize, he notes.

Screenshot

This is true for Singapore-based manager CapitaLand Investment, which sees merit in raising both diversified and sector-specific vehicles, but with the addition of country-level focus and currency diversification. Its single-sector fundraises to date have included Japanese yen-denominated funds focused on office and logistics in Japan, China-focused RMB funds targeting offices and business parks, a rupee-funded vehicle focused on Indian logistics and an India-focused business park development fund in Singaporean dollars.

Simon Treacy, the firm’s chief executive officer for private equity real estate, says offering various combinations of products helps investors to diversify in terms of real estate market cycle, too.

“One market might be on the way up, and another might still be facing headwinds at any given time. But together, you have diversification – that kind of balancing effect which, in their analysis, would make more sense than having three or four investments all in the same types of funds that have the same underlying economic and real estate fundamentals behind them,” he says.

According to Cowins, currency is a point of contention for many. “Making one investment in one jurisdiction and having to deal with a specific currency risk is not going to work for many large, global funds. There needs to be a certain size of opportunity to enable that to be a sensible investment decision,” he says.

As a result, sector-specific funds targeted at a single country – or at least a single currency or region – “would be the most straightforward to raise right now.” He observes particular success for single-country funds targeting residential, logistics or life sciences in today’s market.

Early in 2024, while some participants PERE spoke with see real estate fundraising momentum beginning to recover, others think it will remain sluggish. What they do agree on, however, is that investors will be more selective in their commitments, an approach that will continue to drive capital to the sector specialists.

Importantly, however, this will not be at the expense of the very largest diversified funds, given their increasingly strong thematic focus, solid performance track record and position of trust in the industry. Instead, “the investors that used to invest with the mid-market generalists will split their capital – some will continue to move up the scale to the mega-funds and some will move down, or across, and find the specialists,” says Jacobs.

“I think there’s a very good story for the specialists in the current market. But it’s not so much the fact you’re a specialist which means you’re going to raise money – you’ve got to be a specialist in a market that’s attractive to investors.”

Make it bespoke

To solve for targeted sector exposures, separately managed accounts and joint ventures are increasingly appealing routes for investors

According to Michael Hoffmann, founder of capital advisory Prospective Advisors, some investors looking to fill specific gaps in their portfolios will be more likely to do so in the form of a joint venture or separately managed account than a sector-specific fund.

“We’re out with potential JVs or SMAs in manufactured housing at the moment, we’re doing Mexican industrial – those are very niche,” says Hoffmann. “Investors like the potential for higher returns from these sectors. But what they really like is an ability to say, I want less leverage, or I see an arbitrage opportunity, so I want to build a portfolio quickly and lever it more aggressively to capitalize on that arbitrage potential and generate a quick multiple.”

The process of deciding which type of investment vehicle is most appropriate for an investor is like twisting a Rubik’s Cube, says CapitaLand’s Simon Treacy. It depends entirely on an individual investor’s approach to portfolio construction.

“Understanding the level of discretion an investor wants can evolve into an agreement on a separate account of one, or maybe they feel comfortable with one or two other like-minded investors coming into the same fund where the manager may have discretion, but they require certain approval rights that you wouldn’t ordinarily get in a diversified fund,” he says.

Hoffmann observes that investors that receive performance-based compensation – such as many of the Canadian and northern European institutions – tend to favor SMAs because they can show they made the investment decision and created that strategy with the team. The majority of US pension funds, however, are not aggressively compensated on performance, “making it easier for them to jump into the next Blackstone or other large fund.”